Home | About | FAQ | Intake Form | Resources | Para Hispanohablantes | Blog | Volunteer

Original Medicare + Medigap vs. Medicare Advantage: How to Compare Your Options

Choosing Medicare coverage is one of the most important healthcare decisions many people make when they become eligible for Medicare. Two of the most common options are:

- Original Medicare paired with a Medigap policy and a Part D prescription drug plan

- Medicare Advantage plans

Both options provide Medicare coverage, but they work differently. The right choice depends on your healthcare needs, budget, doctor preferences, and how you like to receive care.

This article is designed for people who are newly eligible for Medicare and do not have other coverage such as retiree insurance, VA benefits, TRICARE, or programs that help pay Medicare costs.

Understanding the Two Medicare Paths

Option 1: Original Medicare + Medigap + Part D

Original Medicare includes:

- Medicare Part A (hospital insurance)

- Medicare Part B (medical insurance)

Many people who choose Original Medicare also purchase:

- A Medigap policy to help pay out-of-pocket costs

- A standalone Part D plan for prescription drug coverage

With this option, Medicare remains your primary insurance, and the Medigap policy helps cover expenses such as deductibles, copayments, and coinsurance.

Option 2: Medicare Advantage (Part C)

Medicare Advantage plans are offered by private insurance companies approved by Medicare. These plans combine Part A and Part B coverage and usually include prescription drug coverage.

Many Medicare Advantage plans also include additional benefits such as:

- Dental coverage

- Vision benefits

- Hearing services

- Fitness programs

Each plan has its own provider network, costs, and rules for receiving care.

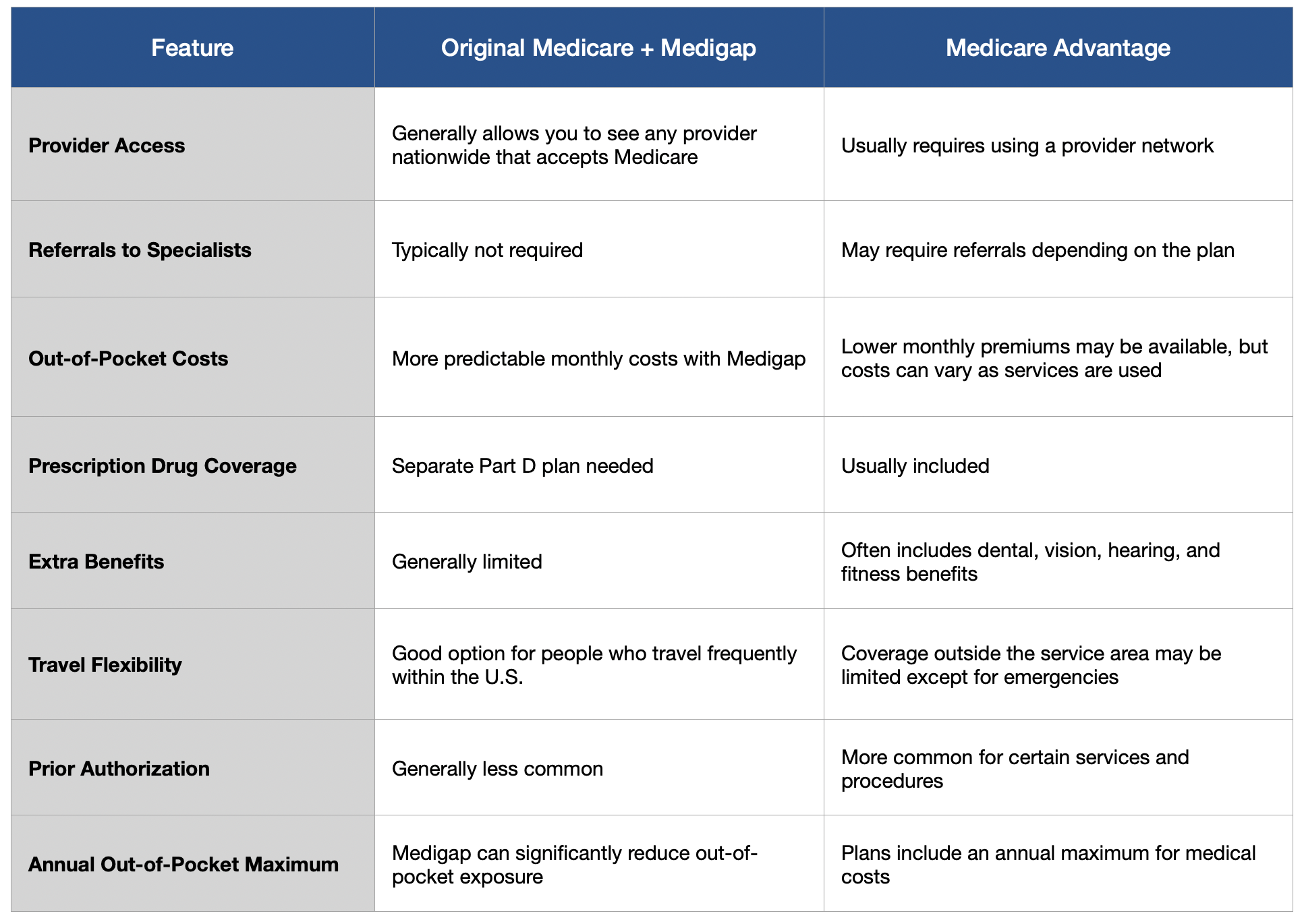

Side-by-Side Comparison

Factors to Consider When Comparing Your Options

Your Current Health Needs

People with ongoing medical conditions or frequent specialist visits may want to carefully review:

- Access to specialists

- Hospital choices

- Treatment authorization requirements

- Expected out-of-pocket costs

Someone who rarely visits the doctor may prioritize lower monthly premiums, while someone who receives frequent care may value broader provider access and more predictable costs.

Access to Doctors and Specialists

Before enrolling in any Medicare coverage option, check whether your:

- Primary care physician…

- Specialists…

- Preferred hospitals…

- Healthcare systems…

…participate in the plan you are considering.

With Original Medicare, most providers nationwide who accept Medicare can be used. Medicare Advantage plans typically use provider networks that may vary by county and plan.

Provider access can be especially important for people who:

- See multiple specialists

- Receive care at specialty hospitals

- Spend part of the year in another state

Understanding Costs Beyond Premiums

Monthly premiums are only one part of the overall cost of healthcare coverage.

When comparing plans, consider:

- Deductibles

- Copayments

- Coinsurance

- Prescription drug costs

- Maximum out-of-pocket limits

Some people prefer paying higher monthly premiums in exchange for more predictable medical expenses. Others may prefer lower monthly premiums and are comfortable with paying for services as they use healthcare.

Prescription Drug Coverage

Prescription drug coverage works differently depending on the option you choose.

- Original Medicare requires enrollment in a separate Part D plan

- Most Medicare Advantage plans include drug coverage

It is important to confirm that:

- Your medications are covered

- Your pharmacy participates

- Your drug costs are reasonable under the plan

- Plan formularies and pharmacy networks can change from year to year.

Travel and Lifestyle Considerations

People who travel frequently or live in multiple states during the year should review how coverage works away from home.

Original Medicare generally offers nationwide access to providers who accept Medicare. Medicare Advantage plans may have more limited routine coverage outside the local service area.

Emergency and urgent care are typically covered nationwide in Medicare Advantage plans, but routine care rules may differ.

There Is No One-Size-Fits-All Medicare Choice

Both Original Medicare with Medigap and Medicare Advantage can work well depending on a person’s healthcare needs and priorities.

A good Medicare decision often starts with asking:

- How often do I use healthcare services?

- Do I want flexibility in choosing providers?

- Are my doctors in the plan’s network?

- How important are predictable costs?

- Do I travel frequently?

- Am I comfortable managing referrals or prior authorization requirements?

Reviewing your healthcare usage, prescriptions, and provider preferences can help you compare options more effectively.

Because Medicare plans and personal healthcare needs can change over time, it is also important to review coverage choices annually.

Need Help Understanding Medicare Options?

Medicare decisions can feel overwhelming, especially when comparing costs, provider access, and coverage rules.

The State Health Insurance Assistance Program (SHIP) provides free, unbiased Medicare counseling to help people understand their Medicare choices and compare coverage options based on their individual needs.

Learn more at AzSHIP.org or call 800-432-4040 to speak to a counselor in your county.

Contact Us

Area Agency on Aging (AAA) is a private non-profit agency, designated by the state to address the needs and concerns of all older persons at the regional and local levels.

The Senior Medicare Patrol (SMP) program is dedicated to safeguarding Medicare beneficiaries, their families, and caregivers from healthcare fraud, errors, and abuse. SMP does this through outreach, education, and counseling.

FUNDING STATEMENT: This project is supported by the Administration for Community Living (ACL), U.S. Department of Health and Human Services (HHS) as part of a financial assistance award totaling $844,187 with 100 percent funding by ACL/HHS. The contents are those of the author(s) and do not necessarily represent the official views of, nor an endorsement, by ACL/HHS or the U.S. Government.

PHONE: 800-432-4040